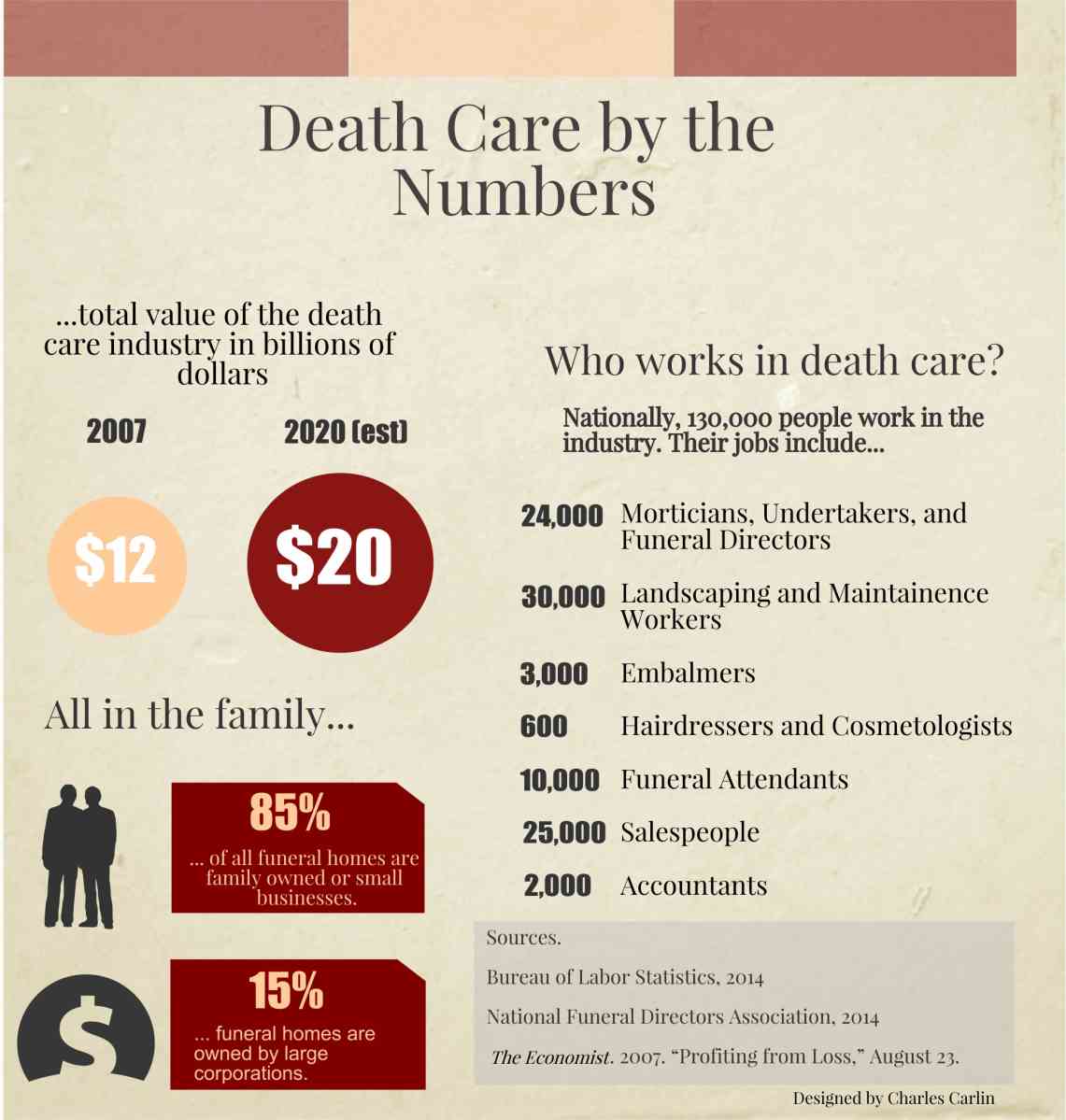

The business of running funeral homes and cemeteries is just that, a business. While some cemeteries like Forest Hill are publicly owned, funeral homes are nearly all private businesses. The American “death care industry,” as it is commonly called, produced nearly 12 billion dollars in economic activity in 2007, and that number is expected to climb to nearly 25 billion dollars by 2020. ((Douglas A. McIntyre, “The Ten Companies That Control The Death Industry,” 247wallst.com, January 13, 2011, http://247wallst.com/investing/2011/01/13/the-ten-companies-that-control-the-death-industry/.)) These numbers include the costs of caskets and headstones, the wages of the cemetery laborers who dig the graves and maintain the grounds, the salaries of funeral directors, and equipment such as crematoria or embalming fluid.

The Death Care Industry by the Numbers

Funerals are expensive. Today, the average funeral costs over $8,000 but often exceed $10,000. By comparison, funeral costs averaged $708 in 1960, which in today’s dollars would be about $5,600. ((Trends and Statistics” (National Funeral Director’s Association, March 9, 2015), http://nfda.org/about-funeral-service-/trends-and-statistics.html#FSF.)) Opting for cremation can lower a funeral cost to around $3,500, which is one reason why cremations are becoming more popular. For more information about concerns related to the costs of funerals and the ethics of the death care industry click here.

Worth over $10 billion and employing more than 130,000 people, death care is big business.

The Bureau of Labor Statistics estimates that around 130,000 people work in the death care industry in the United States. ((“May 2014 National Industry-Specific Occupational Employment and Wage Estimates: NAICS 812200 – Death Care Services” (Bureau of Labor Statistics, May 2014), http://www.bls.gov/oes/current/naics4_812200.htm.)) It takes more than just funeral directors, the people who oversee the process of preparing a body for burial and the funeral service, to make the industry run. Landscapers, monument makers, bereavement counselors, accountants, florists, hearse drivers, janitors, advertisers, security guards, and more all contribute to the functioning of the death care industry. While most of these workers will be employed by privately owned companies, some will be public employees. For example, if the cause of death is uncertain, a coroner employed by the city or the county may investigate. If a person will be buried at Forest Hill cemetery, the backhoe operator who digs the grave will be a city employee. Click here to learn more about a body’s journey to its final resting place at Forest Hill.

The Bureau of Labor Statistics does not keep aggregate data on the Wisconsin death care industry, but some numbers are available for individual occupations. ((“Occupational Employment Statistics: May 2014 State Occupational Employment and Wage Estimates Wisconsin” (Bureau of Labor Statistics, May 2014), http://www.bls.gov/oes/current/oes_wi.htm.)) As of 2013, the Wisconsin economy supported 790 morticians, undertakers, and funeral directors. Around 60 people in the state held jobs as funeral service managers, people who work as the business directors of funeral homes. One can make a good living as a funeral service manager. The mean wage is around $80,000 and the highest paid managers in the state earn close to $140,000. Another 500 people make their living as funeral attendants. They carry the caskets, arrange flowers, organize receptions, and do other support work that makes funerals and burials possible.

Funeral homes: a family affair

While many industries are busy consolidating ownership into fewer and fewer hands, most businesses in the death care industry continue to be family-owned or small businesses. Over 85 percent of the roughly 20,000 funeral homes in the country are privately owned. ((“Profiting from Loss; America’s Funeral Homes: Will Corporations Ever Dominate the ‘Death-Care’ Business?,” The Economist (US), 2007.)) Many death care employees, however, belong to an aging demographic. Funeral home directors tend to be over 55 and many in the industry feel anxious about recruiting enough younger people to replace these directors when they retire. ((Barbara B. Buchholz, “An Ailing Industry The Expected Shortage Of Morticians Puts Those In The Funeral Business On Crisis Alert,” Chicago Tribune, March 18, 2001, http://articles.chicagotribune.com/2001-03-18/business/0103180485_1_funeral-industry-mortuary-colleges-shortage.)) One factor discouraging new recruits may be that funeral directors work long and irregular hours because they must respond to calls at all hours of the day. ((William Clark, Cress Funeral Services, in person, March 25, 2015.)) Statistics about cemetery ownership are harder to come by. There are more than 120,000 cemeteries in the United States and while some are privately owned, many are owned by municipalities, religious institutions, families, or non-profit organizations. ((Kit R. Roane, “Burial Plots: Cemetery Abuses Mean Your Loved Ones May Not Be Resting Where You Think.,” U.S. News & World Report, 2002.))

So who runs the fifteen percent of the industry not controlled by small businesses? Service Corporation International (SCI), a publicly traded company based in Houston, Texas controls nearly all of the fifteen percent of the funeral home industry not held by small companies or families. ((Paul M. Barrett, “Is Funeral Home Chain SCI’s Growth Coming at the Expense of Mourners?,” BloombergView, October 24, 2013, http://www.bloomberg.com/bw/articles/2013-10-24/is-funeral-home-chain-scis-growth-coming-at-the-expense-of-mourners)) They own more than 1600 funeral homes and nearly 500 cemeteries across the country. ((Tom Gara, “More Consolidation in the Deathcare Business,” The Wall Street Journal, May 29, 2013, http://blogs.wsj.com/corporate-intelligence/2013/05/29/more-consolidation-in-the-deathcare-business/.)) SCI owns five cemeteries here in Wisconsin, including Memorial Park Cemetery in Brookfield, one of the state’s largest. SCI does not own any funeral homes in Wisconsin because of a Wisconsin law, discussed below, banning a single owner from operating both a cemetery and a funeral home. ((Rick Romell, “Service Corporation International Sells Schramka and Molthen-Bell Funeral Homes,” Milwaukee – Wisconsin Jounral Sentinel, October 8, 2014, http://www.jsonline.com/business/service-corporation-international-sells-schramka-and-molthen-bell-funeral-homes-b99366857z1-278521551.html.))

While a wave of consolidation ran through the death care industry in the late 1980’s and early 1990’s, it has not turned out to be as profitable as corporations like SCI had hoped. The Economist reported that SCI’s strategy had been to “grow by acquisition and cut costs through consolidation.” ((“Profiting from Loss; America’s Funeral Homes: Will Corporations Ever Dominate the ‘Death-Care’ Business?,” 59.)) During the rush to buy up independent funeral homes SCI and others appear to have both overpaid for the businesses they purchased and overestimated the amount of savings they could generate. This resulted in SCI taking on too much debt, a problem that the Great Recession compounded. However, they have recently resumed acquiring many funeral homes and cemeteries across the country. While their reach is limited here in Madison, in communities like West Palm Beach, Florida, SCI owns more than 60 percent of the area’s funeral homes. ((Barrett, “Is Funeral Home Chain SCI’s Growth Coming at the Expense of Mourners?”))

One reason for the staying power of small businesses in the death care industry is their geographic specificity. Cress Funeral and Cremation Services, for example, maintains eight locations in Wisconsin and three of their facilities are located here in Madison. You may notice the Cress facility on Speedway Avenue across the street from Forest Hill cemetery. Bill Clark, a funeral director at Cress, reports that families tend to look for a funeral home in their neighborhood, which is one reason why many smaller funeral service businesses remain. ((Clark, Cress Funeral Services.)) Madison supports at least twelve different funeral homes scattered around the city. Consolidating multiple funeral homes into a central location may push away potential customers.

Cress has built their business by acquiring other family-owned funeral homes in the area. They purchased the Speedway location from the Frautschi family in 1977. The Frautschis had run a funeral home business in Madison since 1869. Six other Cress locations were also purchased from family-owned funeral home businesses. Clark said that across their eight locations, their company handles about 1300 deaths each year. This is significantly higher than the 113 deaths per year that the average funeral home manages. ((“Trends and Statistics.”)) Owning eight funeral homes allows a local company like Cress to emulate some of the strategies that corporations like SCI employ. For example, while Cress maintains several facilities in Madison, all the preparation of bodies and cremations happen at one location.

Choosing between cemeteries and funeral homes: the Wisconsin Co-ownership Law

Geographic specificity raises the question, why not offer funeral home services at cemeteries? Many states take that approach, but Wisconsin prohibits the practice. Since the 1930’s, Wisconsin law has banned a single company from owning both funeral homes and cemeteries. ((“CHAPTER 157: DISPOSITION OF HUMAN REMAINS” (Wisconsin State Legislature), accessed April 8, 2015, http://docs.legis.wisconsin.gov/statutes/statutes/157/II/064.)) Nine states have similar laws, though Wisconsin’s is one of the strictest.

The law has been a subject of contention between funeral directors and cemetery owners. Cemetery owners claim that they need to have access to increased revenue streams due to increasing financial stress. ((Rick Romell, “Time for Cemetery Law to Die?,” Milwaukee – Wisconsin Jounral Sentinel, January 15, 2012, http://www.jsonline.com/business/states-funeral-homes-cemeteries-fight-over-turf-bp3prhd-137370618.html.)) Many cemeteries are funded through an endowment and returns on investments pay a substantial portion of their operating costs. Each time the stock market drops sharply, as in 2008, the financial health of cemetery endowments is put at risk. Furthermore, with cremation now more popular than burial, fewer people are purchasing space in cemeteries and those who do often buy smaller plots.

Funeral directors, however, support the law, claiming cemeteries that also run funeral homes would have an unfair advantage. They give two main reasons. First, cemeteries tend to pay reduced property tax rates. ((Clark, Cress Funeral Services.)) Second, while cemeteries often have space to accommodate funeral home facilities, it would be much more difficult for a funeral home operator to buy a large chunk of land inside city limits to enter the cemetery market. ((Rick Romell, “Ban on Co-Ownership of Cemeteries, Funeral Homes Challenged,” Milwaukee – Wisconsin Jounral Sentinel, September 3, 2014, http://www.jsonline.com/business/challenge-planned-to-state-ban-on-co-ownership-of-cemeteries-funeral-homes-b99344190z1-273848271.html.)) At least in the short term, abolishing the co-ownership law would benefit cemetery owners more than funeral home operators.

Since the 1980’s, cemetery owners have repeatedly pushed to have the co-ownership law overturned. Legislation to overturn the law has been introduced in the Wisconsin statehouse at least four times. It has failed to pass each time. In the fall of 2014, the owners of Highland Memorial Park cemetery in New Berlin, Wisconsin filed a lawsuit challenging the constitutionality on the cross-ownership ban. Their lawsuit claims that the law unduly restricts their right to earn a living guaranteed by the due-process and equal-protection clauses of the Wisconsin Constitution. ((Ibid.)) As of this writing, the lawsuit has not been resolved.

Cremation trends

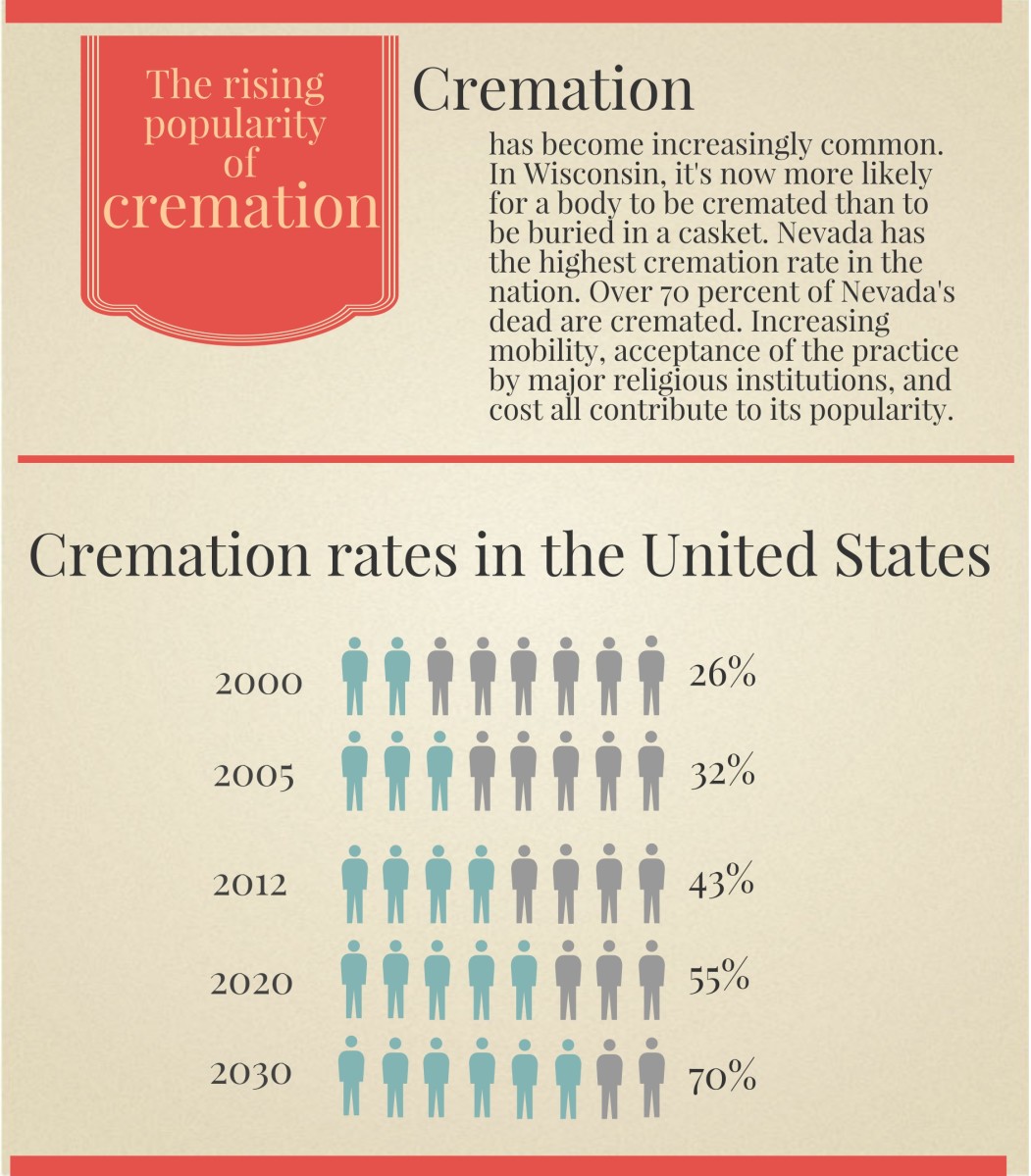

In Wisconsin, more people now choose to be cremated than buried. The National Funeral Directors Association estimates that in 2015 about 54 percent of Wisconsinites who die will be cremated. Around 38 percent will have their bodies buried in a casket. Others will choose to be entombed in a mausoleum, to donate their body to science, or to be buried at sea. Wisconsinites may be disappointed to know that burial in the great lakes is not an option as burial at sea is only legal in international waters. Nationally, more and more people are choosing cremation. In 2000, only about 26 percent of bodies were cremated. Now, over 45 percent choose to be cremated and it is estimated that by 2030 over 70 percent of Americans will choose to be cremated when they die. ((“Trends and Statistics.”))

Economics, demographics, and shifting religious attitudes all seem to be driving the trend towards increasing cremation. First, cremation can be far less expensive. While a traditional funeral and burial often surpasses $10,000, cremation can be done for less than a third of that amount. Even more significant than economic pressures are demographic changes. First, American families move around much more than they used to. Therefore, fewer families now purchase a family plot in a cemetery like Forest Hill where they expect to be buried together. ((Clark, Cress Funeral Services.)) Cremating a body allows a family to schedule a memorial service when everyone can come together. Embalming, on the other hand, can only keep a body presentable for a week or two. Also, in the 1990’s the Catholic Church began allowing cremated remains at Catholic funerals, which has led to increased cremation rates among Catholics. ((Daniel Gross, “Weep for the Grim Reaper,” Slate, November 9, 2007, http://www.slate.com/articles/business/moneybox/2007/11/weep_for_the_grim_reaper.html.)) Overall, fewer Americans now participate in organized religion, and this seems to be producing less demand for traditional funerals and burials. ((Public Sees Religion’s Influence Waning,” Pew Research Center’s Religion & Public Life Project, September 22, 2014, http://www.pewforum.org/2014/09/22/public-sees-religions-influence-waning-2/.)) Cremation allows families to craft their own services and scatter ashes where they choose. Some claim that we are running out of cemetery space, but that appears to be less of a concern here in Madison. ((“Too Many Bodies, Too Little Space,” The New York Times, accessed February 13, 2015, http://www.nytimes.com/roomfordebate/2013/10/30/cemeteries-are-running-out-of-room/baby-boom-will-lead-to-shortage-of-cemetery-space.)) Forest Hill still has burial and cremation plots as well as mausoleum space available.

Back to Top | Geography of Death Main Page | Muckraking and Consumer Protection | Dane County’s Death Investigation Unit | Zoning